Should you’re searching for efficient methods for making sound inventory choice choices, you possibly can do rather a lot worse than peep into the present portfolios of Wall Avenue’s investing titans. By discovering which equites they’re leaning into at any given time, traders can piggyback on the decades-long success attained by the inventory choosing giants.

Few are extra profitable at this recreation than Ken Griffin, the founder and CEO of hedge fund Citadel and a person with a internet value of ~$34 billion. Final yr, towards a backdrop of a cruel bear market, Citadel raked in file income of $16 billion, a testomony to Griffin’s and the agency’s market expertise.

With this in thoughts, we used TipRanks’ database to search out out what the analyst group has to say about two shares that Griffin’s fund snapped up lately. It seems that the analyst consensus has rated every a “Sturdy Purchase.” To not point out stable upside potential can also be on the desk. Let’s take a more in-depth look.

Mobileye World (MBLY)

Griffin has evidently been eying the shift going down within the auto business. Mobileye World is a distinguished chief within the realm of superior driver help methods (ADAS) and autonomous driving expertise. The agency was based in 1999, and has since developed right into a globally acknowledged pressure, revolutionizing the automotive business with its cutting-edge improvements. Specializing within the improvement of vision-based options, the corporate focuses on equipping autos with state-of-the-art cameras and sensors that allow a better stage of security, effectivity, and automation on the roads.

Mobileye was snapped up by Intel in 2017 however was spun off final October in a blockbuster IPO. Since then, the corporate has made a behavior of beating bottom-line expectations in its quarterly readouts, a development that continued in July’s Q2 report.

The corporate delivered adj. EPS of $0.17, beating the Avenue’s forecast by $0.05. Though income skilled a 1.3% year-over-year decline to $454 million, this determine nonetheless exceeded the consensus estimate by $3.14 million. Wall Avenue, nevertheless, was not all that impressed, as the corporate maintained its full-year income outlook, anticipating gross sales to fall throughout the vary of $2.07 to $2.11 billion. The mid-point of this vary falls simply in need of the $2.1 billion expectation set by analysts.

Griffin, although, should see loads of worth right here. His fund opened a brand new place in the course of the quarter, buying 2,415,297 shares. These are presently value $92 million.

Wanting on the firm’s prospects, it’s the chance afforded by Mobileye’s most superior driver-assist system SuperVision, that informs Canaccord analyst George Gianarikas’ bullish take.

“The all-important SuperVision product rollout stays on observe, with the corporate reaffirming its 2023 and 2024 unit estimates and anticipated inflection level in 2026. Whereas our assumption of 220k SuperVision unit shipments in 2024 stays intact, we suspect some fashions might have had a better estimate and never adjusted for the recalibration from 1Q23. The corporate continues to see robust OEM curiosity in SuperVision and expects ‘critical engagements’ with many OEMs to mature into further design win bulletins by the tip of the yr,” Gianarikas famous.

“We see Mobileye’s full built-in, system stage method, together with REM mapping and RSS, mixed with billions of miles of mapping knowledge and near twenty years of R&D, as tough to surmount long run,” Gianarikas went on so as to add.

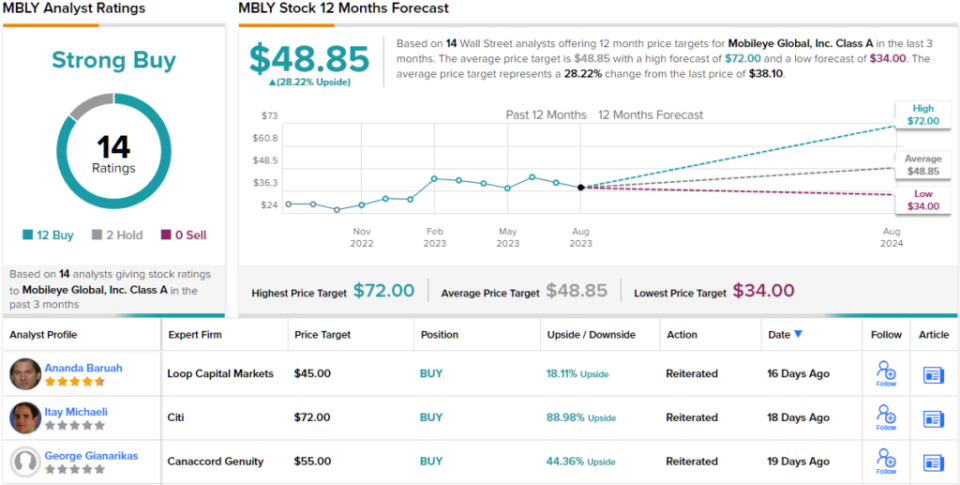

Accordingly, Gianarikas charges MBLY inventory a Purchase whereas his $55 value goal implies one-year share appreciation of 44%. (To look at Gianarikas’ observe file, click here)

Most analysts agree with that stance. Primarily based on 12 Buys vs. 2 Holds, the inventory claims a Sturdy Purchase consensus score. At $48.85, the typical goal makes room for 12-month returns of ~28%. (See MBLY stock forecast)

Acelyrin, Inc. (SLRN)

For our subsequent Griffin-backed choice, we’ll change lanes and pivot to the biotech house. Acelyrin is a late-stage biopharma targeted on creating transformative therapies for sufferers.

The corporate is a relative newcomer to the inventory market, having held its IPO in Might of this yr. The general public itemizing was an outright success, with the upsized IPO elevating $621 million for the corporate, making it the biggest biotech IPO within the US since early 2021.

Evidently, the corporate’s pipeline is popping heads. ACELYRIN is presently engaged on three medicine, all in numerous phases of improvement.

Its lead candidate is izokibep, an IL-17A inhibitor being put via late-stage testing as a therapy for hidradenitis suppurativa, uveitis and psoriatic arthritis.

Prime-line knowledge from the placebo-controlled Half B of the Part 2b/3 trial of izokibep in hidradenitis suppurativa is anticipated to see the sunshine of day someday within the third quarter. Moreover, a top-line knowledge readout from the part 2b/3 randomized managed trial of izokibep in psoriatic arthritis lately obtained pushed ahead to 1Q24 from mid-2024.

Elsewhere within the pipeline, lonigutamab is being developed as a therapy for thyroid eye illness (TED) with top-line outcomes from the continuing Part 1/2 Proof-of-Idea (PoC) trial anticipated in late 2023/early 2024.

Lastly, the Part 1/2 PoC trial of SLRN-517 in continual urticaria (CU) can also be going down proper now. Prime-line outcomes from this research are anticipated within the second half of 2024.

Griffin has been fast in figuring out the potential right here, and through Q2, his fund snapped up 6,039,657 shares, which presently command a market worth of just about $163 million.

With a number of readouts deliberate for the pipeline, Piper Sandler analyst Yasmeen Rahimi additionally has excessive expectations.

“We foresee the corporate turning into a pioneer within the inflammatory illness house,” Rahimi stated. “Past an distinctive administration workforce, SLRN is presently creating 3 medicine, which all have validated MoAs: 1) izokibep (IL-17A inhibitor); 2) lonigutamab (anti-IGF-1R); and three) SLRN-517 (anti-c-KIT). Impressively, every asset has pipeline-in-a-product potential with indication enlargement alternatives into further blockbuster indications. Looking forward to the following ~yr, SLRN has 10 direct catalysts and 25 oblique catalysts, which we consider will probably be key stock-moving occasions to in the end drive shares up.”

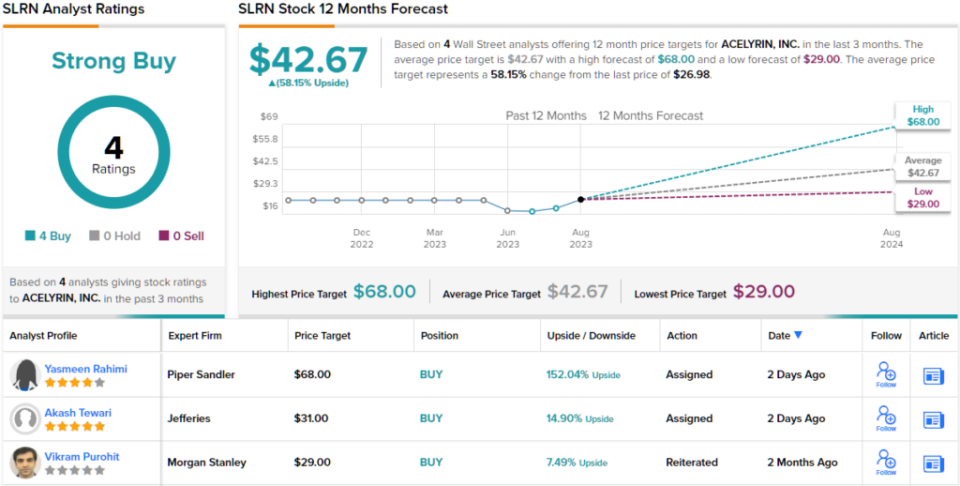

Up, certainly. Together with Rahimi’s Chubby (i.e., Purchase) score, her $68 value goal suggests shares will climb 152% larger over the approaching yr. (To look at Rahimi’s observe file, click here)

Total, SLRN inventory has garnered 4 analyst critiques lately and all are constructive, making the consensus view right here a Sturdy Purchase. The forecast requires one-year returns of 58%, contemplating the typical goal stands at $42.67. (See SLRN stock forecast)

To seek out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Best Stocks to Buy, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely necessary to do your personal evaluation earlier than making any funding.