[ad_1]

Depending on the company you work for, your compensation may include some form of equity — likely stock options or restricted stock units (RSUs). In this post, we’ll explain what they are, how they differ, and why you’re likely to be granted fewer RSUs than stock options (all other things being equal).

What are stock options and what do they mean?

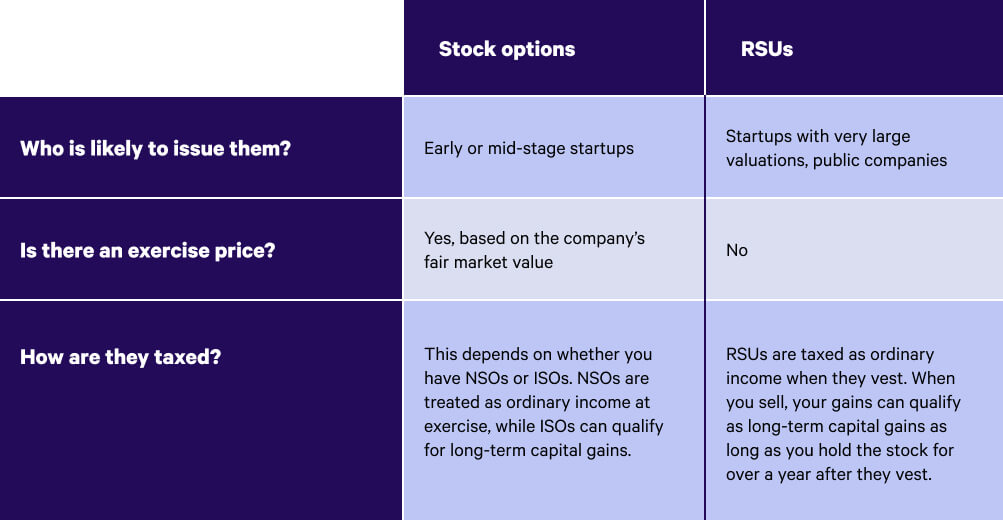

Employer-granted stock options allow you to buy stock from a company at a specified price and time. The act of buying the stock is known as exercising your options. The price you’ll pay to do that is called the exercise price or strike price — this price is set when you are granted your options. Stock options granted by employers can be incentive stock options(ISOs) non-qualified stock options(NSOs) are subject to varying tax treatment (more below). Stock options are frequently subject to vestingThis means that you might need to work for the company for a while before you can exercise any of your options.

What are RSUs and how do they work?

RSUs are shares of stock that employees can claim as compensation. Unlike stock options, you don’t have to pay to exercise RSUs — once they vest, they’re yours. RSUs were more common among employees of public companies in the past than for those working at private companies. But over the last 20 years, RSUs have become much more common at private companies that have closed rounds of financing at large valuations (over $1 billion) when that valuation isn’t likely to be achieved or justified for a few years. RSUs, like stock options are subject to vesting.

Stock options vs. Registered Student Unions

Here’s a breakdown of the key differences between stock options and RSUs:

Stock options and RSUs have different tax treatment

Equity compensation can make your tax situation more complicated, and it’s important to understand what you could owe. Let’s take a closer look at the tax treatment of stock options and RSUs.

How RSUs can be taxed

RSUs are subject to tax as soon they become liquid or vest. Most cases, your employer will withhold some RSUs to cover taxes owed at vesting. In some cases, you might be able to pay the taxes in cash to keep all your vested RSUs. Your RSUs will still be subject to ordinary income tax. could be as high as 37% at the federal levelDepending on your income, you may also owe Medicare and Social Security taxes. Your location may impact whether you owe additional taxes.

How stock options are taxed

Stock options are, however, taxed when they’re exercised or sold. This means that you may want to exercise your options within a year when your tax rate is low, or you have lots of harvest losses to use with an investment manager such as Wealthfront. If you are interested in this, please early exercise your options before they’ve increased in value and file an 83(b) election within 30 days, then you won’t owe any taxes until you sell.

The rest of the tax depends on whether your NSOs are more common or ISOs. NSOs will result in ordinary income rates. This is the difference between the exercise price (or the current fair market value) at the time you exercise. Gains or losses arising from the sale of shares held for longer than one year will be subjected to lower taxes. long-term capital gains rateThis ranges between 0% and 20%. For regular tax purposes, exercising ISOs is not considered a taxable event. Any increase in value over the exercise price will be taxed at the long-term capital gains rate when you sell as long as you meet both of the following conditions:

- You must hold the shares at least for two years after they are granted.

- The shares are yours for at most one year following their exercise

Also, be aware alternative minimum taxIf you have ISOs, AMT is available. AMT is an independent tax system that ensures high-earners pay a minimum amount (hence its name). If you exercise your ISOs and don’t sell them that year, the difference between the exercise price and the fair market value at the time of exercise is subject to AMT even if you didn’t sell any shares. AMT can make filing your taxes far more complicated, which is why we think it’s smart to consider working with a tax professional if you think you might be subject to AMT. Whether or not you pay AMT is largely dependent on your income — in 2021, if you’re a single filer making less than $73,600 or a married couple filing jointly making less than $114,600, you don’t need to worry about it. If you earn more than that, however, you’ll need to calculate your taxes under both systems (AMT and the regular system) and pay whichever amount is bigger. Good news: your AMT payments can be credited against taxes due upon the sale of your options.

Why you’ll get fewer RSUs than stock options for the same job

You should expect to receive fewer RSUs than stock options for the same job because RSUs don’t have an exercise price. Let’s look at a hypothetical private company example to illustrate this. Imagine a company that has 10 million shares outstanding and just closed a $100 per share financing. This would translate to a valuation of $1 billion. If you knew that the company would ultimately be worth $300 per share, then you’d need to issue 11% fewer RSUs than stock options to deliver the same net value to the employee.

Here’s a chart to help you visualize this example:

RSUs are independent of company performance, while stock options may lose their value if they fail. Simply put, RSUs are safer than stock options.

Takeaways: Stock options and RSUs

If you receive equity as part of your compensation, here’s what you need to remember about RSUs and stock options:

- Stock options and RSUs give you the chance to own a part of the company that you work for.

- RSUs don’t have an exercise price, but stock options do — that’s why you’ll receive fewer RSUs than stock options for the same job.

- RSUs offer less flexibility than stock options when it comes tax planning (both rate and timing).

These tips will help you navigate the equity component of your compensation. For more guidance on how to handle RSUs, check out this blog post for our advice on managing vested RSUs — generally, we think it’s smart to sell some portion of your RSUs and invest in a more diversified way (Wealthfront’s Investment Accounts make this easy). For a deep dive on all things related to equity, we encourage you to read Wealthfront’s Guide to Equity & IPOs.